In India, safety always comes first. It comes with an additional cost. How much would you pay for safety and risk free income?

Which is the useful option;investing in shares online or fixed deposits

The topic for discussion here is safe fixed deposits and risky stock market equity investments.

“Risk comes from not knowing what you’re doing” – Warren Buffett

Fixed deposits are term deposits which involve locking in your money for a fixed rate of return for a fixed term. Most people invest their savings in fixed deposits. But can we do better than that?

Equities allow individuals to own businesses listed on exchanges in public markets. Index is a benchmark to track the general performance of listed businesses and often used to calculate returns from equities. In India, Sensex or Nifty are the major indices that people track.

Let us analyse through this article the pros and cons of investing in fixed deposits vis-a-vis stock market.

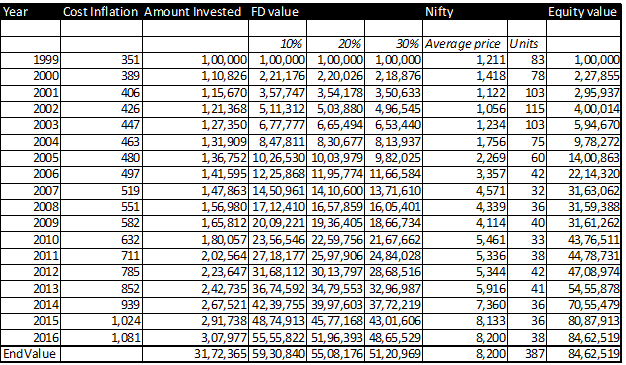

Anything that cannot be measured cannot be improved. So let us start by studying historical data to find out which has proved to be better investment in terms of returns in the longer term. The below table assumes one started investing with INR 1 Lakhs and increased the investment amount proportionately with cost inflation index. Cost Inflation Index is a measure of inflation that is used for computing long-term capital gains on sale of capital assets. The table compares the cumulative value of investments for different tax slabs in fixed deposits and equities on an annual basis. In India, the tax applicable on fixed deposits is as per one’s income tax slab and on equities long term capital gains tax is zero. Long term is defined as investment above one year.

Always Do Better Investment Start Investing In Equities

FD Rates since 1999

Results of the above table

- Total amount invested over the period 31.72 Lakhs

- 84.62 Lakhs in equities is the final amount irrespective of the tax slab

- 50-60 Lakhs in fixed deposits is the final amount depending on tax slab

Equity value under performs in the initial years (in our data set till 2004) but post 2004 equities outperform the fixed deposit investments till date. The return is far greater in equities compared to fixed deposits over the long run. An important thing to note here is the volatility is higher in the initial years of equity investments, but after five years the returns for equities are significantly higher and relatively stable.

The data set in the above example, contains the higher end of fixed deposit rates over the period and average price of Nifty in that year. The numbers are based on data available on RBI and NSE website and may have some approximation but the conclusion is quite clear. Equities in the longer term should be the clear choice in one’s portfolio.

Imagine your neighbor’s kid inheriting more than 50% wealth just because his parents invested in equities all along while you were booking fixed deposits. Would you be able to explain to your child the reason for this ignorance? Does your kid deserve a better future? Probably yes. Is it too difficult to comprehend? Probably no.

Fact box :-

According to a Bloomberg article from Apr, 2015 less than 1.5% of Indian households invest in equities compared with 10% in China and 18% in the USA. Just 2% of household savings are exposed in equities vs 45% in the USA. The Sensex gave a return of 17 percent compounded annually between August 2004 and August 2014. That’s twice as much as Indians earn from their most preferred mode of financial savings: bank deposits.

Warren Buffet Says :-

“The worst investment you can make over time: cash”

We always keep enough cash around so I feel very comfortable and don’t worry about sleeping at night. But it’s not because I like cash as an investment. Cash is a bad investment over time. But you always want to have enough so that nobody else can determine your future essentially. So start investing in stock market.

Invest in a broad-based index fund that tracks the S&P 500.

If you are a professional and have confidence, then I would advocate lots of concentration. For everyone else, if it’s not your game, participate in total diversification. The economy will do fine over time. Make sure you don’t buy at the wrong price or the wrong time. That’s what most people should do, buy a cheap index fund, and slowly dollar cost average into it. If you try to be just a little bit smart, spending an hour a week investing, you’re liable to be really dumb.

Be careful in interpreting the above. What he is really saying is settling for cash or deposits is really a bad investment to make. The broader economy does well over time and the best way to be a part of it is to systematically invest in it through index/mutual funds. Timing is unnecessary for a retail person and it’s best to diversify it over time and with index funds.

Also Read Facts you may not know about Warren Buffett

Investment planning and Instruments

Equities through Mutual Funds ?

There are a lot of mutual funds in India, which can be bought online by linking your bank accounts through online trading portals or going through stock brokers. Many brokerage firms in India provide mutual fund service through their online trading portals. There are large cap, mid cap or small cap focussed funds which invest your money based on the size of companies. Also, there are sectoral funds which invest is specific sectors like banking, infrastructure, IT, exports, etc. Debt mutual funds are separate from equity mutual funds, a combination of debt and equity are balanced funds. Also equity mutual funds are tax efficient and can be used for investment under the Equity Linked Saving Scheme tax deduction plan.

Risk in Equities ?

There are two major risks in life; risking too much and risking too little. The risk stems from the fact that equities should only be considered as an investment for the long term. Any short term outlook is uncertain and generally could end in disappointment or unexpected results. As we saw in the example there is no guarantee whether the equity value of your investments will go up or down in the initial few years.

“We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten. Don’t let yourself be lulled into inaction.” – Bill Gates

“I never attempt to make money on the stockmarket. I buy on the assumption that they could close the stock market the next day and not reopen it for five years.” – Warren Buffett

“Over the long term, the stock market news will be good. In the 20th century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a fly epidemic; and the resignation of a disgraced president. Yet the Dow rose from 66 to 11,497.” – Warren Buffett

So any money that you would require for next 5-7 years should not be channelized into equities. As mentioned above the greatest risk comes from our lack of understanding. One should be clear equities are a great investment in the long term, but could be volatile in the short term.

What is recommended?

Our recommendation is clearly divided the corpus into two halves, one short term and the other long term. Invest most of the long term corpus into equities and keep most of the short term into debt and other instruments. Young people can keep most of their money in equities as their ability to take risk is higher and they have time by their side. Stock trading for beginners is good concept. The work you need to do in the beginning is often very painful and tiring. But once your wealth snowball is built, then your wealth naturally attracts more wealth. Then the power of compounding can work in your favor.

Sir John Templeton says

The four most dangerous words in investing are ‘This time it’s different.’ This is a good one and a hard teaching to master. Investors often play the market psychologically, when they should stick to their strategy on paper, not with emotions. We often make mistakes as investors and instead of learning our lesson, making us savvier investors, we seem to keep committing the same mistakes over and over again. A certain feeling of optimism when the situation repeats arises when the opportunity reappears.

The opportunity is now for the next many years to come. It’s for us to take it.

Also Read How returns from various asset classes are taxed?

[email-subscribers namefield=”NO” desc=”Subscribe now to get latest updates!” group=”Public”]

[…] Also Read : Fixed Deposit v/s Equities – Which is better? […]

[…] Also Read : Fixed Deposit v/s Equities – Which is better? […]

[…] Also Read : Fixed Deposit v/s Equities – Which is better? […]

[…] Also Read : Fixed Deposit v/s Equities – Which is better? […]

[…] Also Read : Fixed Deposit v/s Equities – Which is better? […]

[…] Also Read : Fixed Deposit v/s Equities – Which is better? […]