Cheap oil: check. Low interest rates: check. Benign inflation: check. Easy liquidity: check. Growth: ?

How GDP will affect the share market

Despite lower input prices and relatively stable markets, global economic growth prospects remain subdued. That is if one were to go strictly by the headlines relating to IMF’s latest update to its World Economic Outlook, published on 20 January. Key changes from its original estimates for 2015 and 2016 growth estimates of October 2014:

Data source: IMF

You may wonder: oil prices have been on a southward trajectory since October (declining in USD terms by about 55% since September) and the world was gushing over how great this is going to be for emerging and developed market growth. So what does the IMF have on its mind?

Firstly, the key considerations behind the revisions to the forecasts:

Graphic Source: IMF

What this implies is that stronger than expected growth in the US and weaker growth prospects in China are leading to a realigning of the global economy. Even though China is likely to benefit more from weaker oil prices than the US (due to its domestic oil industry and almost complete self-reliance), the fundamental nature of the Chinese economy lends itself to lower growth rates. China’s economic model relied upon a) export led growth, which has faltered in the face of slowing demand from developed world; and b) capital investment, for which appetite and cash is in short supply.

This realignment is reflected in:

- currency markets (the USD has appreciated 6% in real effective terms since October 2014. In contrast, the euro and the yen have depreciated by about 2 percent and 8 percent, respectively);

- interest rates (emerging market economies and high yield issuers have seen spikes in interest rates even as sovereign yields for countries like USA and Germany are nearing historical lows); and

- equity markets (barring a few exceptions, most equity markets have remained unchanged in the last 3-4 months).

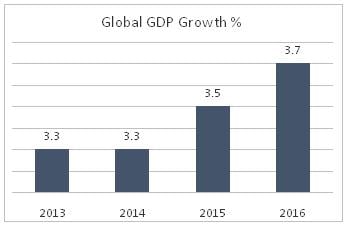

Despite the gloom, the growth trajectory remains an upward one:

Bottom line: growth prospects remain good. The drag on global GDP growth largely comes from commodity exporting countries (Russian, China, OPEC block, etc.) and China.

Bottom line: growth prospects remain good. The drag on global GDP growth largely comes from commodity exporting countries (Russian, China, OPEC block, etc.) and China.

Some developments to watch out for in 2015:

- The growth trajectory in the USA implies that the Fed’s soft stance on interest rates will reverse sooner rather than later. This implies volatile times for global financial markets

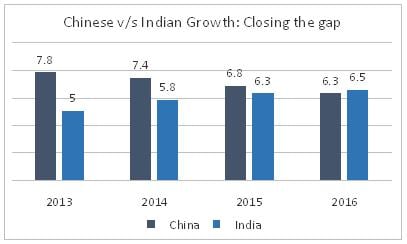

- China’s growth rate (2014 GDP growth came in at 7.4%) is now at a 6 year low with further declines expected in 2015 and 2016 – a slowdown in the world’s growth engine does not augur well for commodity exporting countries that relied on an ever-hungry China

- Contagion effects of a crisis exacerbated by Greece’s exit from the EU-27 could be substantial

- The Japanese and European responses in the form of their own quantitative easing measures will have ramifications for the rest of the world

- Lower revenues for OPEC and other oil exporting countries (Russia, Nigeria, Arab World) could lead to geo-political stress besides reduced portfolio flows.

A few specific takeaways for India:

– India is one of the biggest beneficiaries of low oil prices; gains to begin showing in 2015.

o This gain is however likely to accrue more in fiscal management (lower subsidies) rather than higher consumer purchasing power

– Growth rate to overtake China’s in 2016

o Good for headlines and sentiment

– One of the few countries / regions to not suffer any downward revision to growth prospects

o Key positives are improving fiscal position and expectations of market friendly reforms

With India and the US turning into the world’s most important growth engines, prospects look far from benign – the Indian equity markets have certainly reacted positively to this news. The next big event for the markets will be the Union Budget and going by early indications, it could be a big bang exercise. At the same time, a number of other issues like coal block auction and ordinances on land acquisition & insurance are expected to sail through smoothly while more concrete steps are likely in areas of “Make in India”, subsidy rationalisation and the big idea of ‘Smart Cities’, thereby giving corporate earnings and overall growth the necessary push. More rate cuts are expected and that will only add to the positive sentiment. Clearly, bulls will have enough reformist fodder to chew on in the next few months and keep the rally going!