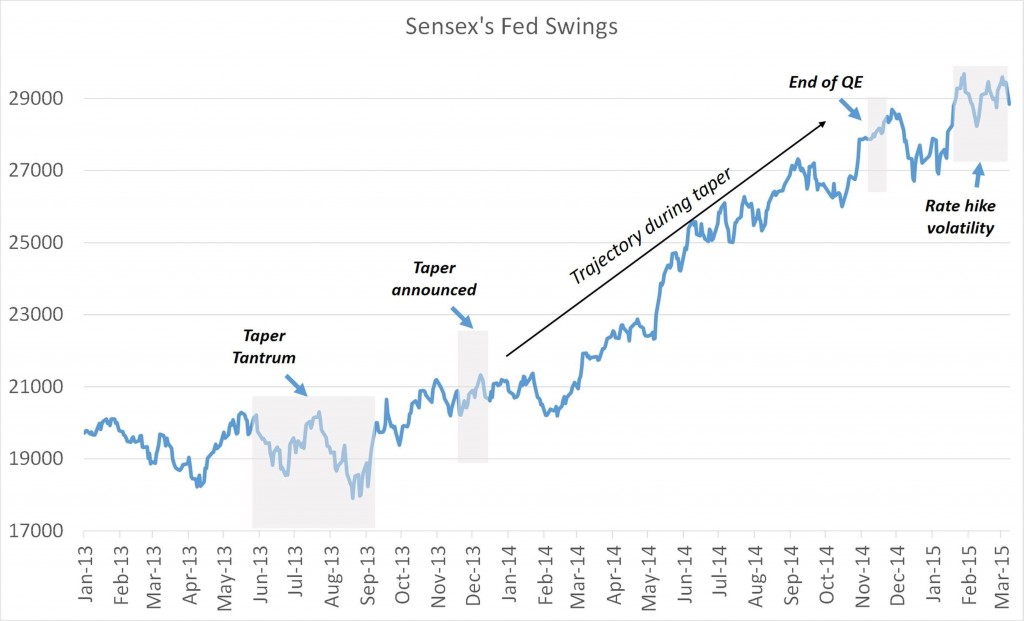

A 600+ point hit on the Sensex despite the Government and RBI’s largesse! Investors just need to ride out the Rate Rant of the markets if the Taper Tantrum was anything to go by.

How rate hike will benefit stock broker

After an excellent start to 2015 despite lackluster Q3 results, stock markets are in a bear hug on stronger signals from the Fed that a rate hike may be around the corner. Earlier, the Fed had indicated that in the absence of an inflation uptick and inconclusive growth indicators, the rate hike may be deferred to mid-2015. Now with US growth numbers looking a lot more stable and the world looking like it may not end soon, the Fed has begun signaling its hawkish intent and stock markets are nervous that the era of cheap money may well be truly over.

Stock Markets like predictability and react most to the unexpected. Like the QE rollback, even the rate hike has been expected. The Fed has done a decent job of signaling and the only aspect that is new is that the stronger than expected US recovery has preponed the potential hike from the announced June 2015 timeline – a move up of a mere 2-3 months. The prospect of a QE taper too had spooked stock markets despite the Fed’s excellent job of expectations management. Where are the markets since the taper began in Jan’14? At the recent peak, the Sensex is up around 55% from the ‘Taper Tantrum’ days – that’s an almost 25% CAGR!

What we see is probably more of an excuse for an over-due correction. The stock market has rallied up significantly (about 9%) since a weak December 2014 and was looking ripe for a fall. Weak corporate results, unreasonably high expectations from the budget, the BJP’s Delhi loss, a stormy budget sessions (entirely expected as it was) – put together, these are substantial. Yet, perhaps the fall is an exaggerated one. Perhaps the fall has been moderated by the surprise rate cut by RBI last week. Perhaps it has further to fall. Calls being made on market levels WITH timelines are an exercise in futility in such a scenario.

What we see is probably more of an excuse for an over-due correction. The stock market has rallied up significantly (about 9%) since a weak December 2014 and was looking ripe for a fall. Weak corporate results, unreasonably high expectations from the budget, the BJP’s Delhi loss, a stormy budget sessions (entirely expected as it was) – put together, these are substantial. Yet, perhaps the fall is an exaggerated one. Perhaps the fall has been moderated by the surprise rate cut by RBI last week. Perhaps it has further to fall. Calls being made on market levels WITH timelines are an exercise in futility in such a scenario.

Some realities around a rate hike by the Fed are a little clearer though:

- As rates are hiked, the risk premium for US investors will rise. This will lead to a rise in expected returns and in its absence, a reduction in flows into risky assets such as Emerging Market equities.

- Some degree of mandated capital outflows will occur as FIIs pull out money from Emerging stock Markets everywhere. However, in the pecking order of things, India’s position with overseas investors has improved considerably since last year on account of strong intent towards reforms and boosting expenditure while maintaining fiscal discipline. Besides, there aren’t that many countries where investors could reasonably expect returns of 15-20%.

- A rate hike will lead to a stronger dollar as investment flows into the US rise. This in turn is good news for India as export competitiveness rises even as a stronger dollar pulls down oil prices.

- The end of the Fed’s QE and rate hike, if it occurs, will coincide with the start of the ECB’s own QE and Japan’s continuation of its home-grown version. These can serve to fill the vacuum and top up the lost cheap money.

India cannot escape the ‘risk off’ trade that will inevitably happen if a rate hike is indeed announced, more so if accompanied by hawkish language for the future. Yet, perhaps the tradition adage sums it up best for the markets – ‘This Too Shall Pass’.