Welcome to the 10th edition of our weekly musings!

The latest data on high-frequency indicators has been encouraging and shows quite a rebound for India’s economy, although India is still not out of the woods as far as the impact of Covid-19 is concerned. Stress faced by India’s MSMEs, rising fiscal deficit, the upward trajectory of inflation, and the unemployment levels remain the key worrying points for India’s $2 trillion economy.

India witnessed a higher trade deficit in October due to a sequential improvement in imports and weaker exports. The re-imposition of lockdowns in European countries as a result of the second wave of coronavirus could add more to India’s trade deficit as the export growth looks soft for the rest of the financial year. India’s October trade deficit stood at US$ 8.8 bn with exports falling by 5.4% against a growth of 6% in September, and imports falling by 11.5% against a decline of 19.6% in September.

RBI’s timely intervention and the conservative approach followed by most NBFCs and Banks have led to India’s financial sector showing some early signs of economic recovery with efficiency in collections, requisite provisioning, and the infusion of fresh capital (Bank recapitalization).

India continues to be one of the favorite destinations among the emerging markets due to the vigorous performance of the rural economy and with the hopes of a possible gain in market share in the manufacturing sector as a result of the anti-China sentiment.

Global equity markets cheer as America declares Joe Biden its projected winner in the Presidential Race

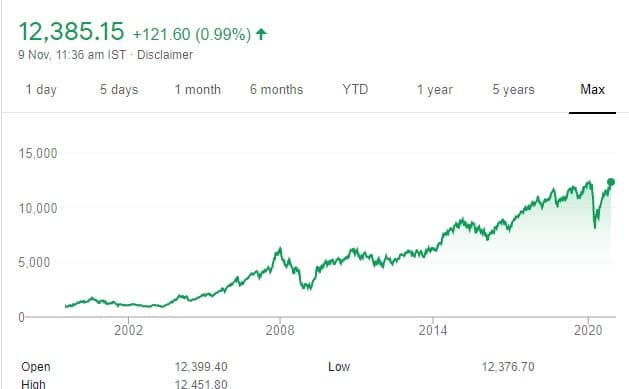

The NSE benchmark, Nifty 50 scaled a fresh life-time high of 12,450 as the bourses opened with the news of Joe Biden securing a majority by winning more than 270 electoral votes and getting himself projected as the winner of US Presidential Elections 2020.

Nifty-50 hits a record high

Source: Google Finance, Tavaga Research

From being the 5th youngest senator to the oldest US President-Elect, Joe Biden has sailed through in the election by crossing the required majority of 270 electoral votes. From the current trends, it has become clearer that the US is likely to continue with its tradition of a divided Congress with the Senate controlled by the Republicans and the House of Representatives under the Democrats.

A blue White House with a Republican Senate will ensure that a hike in taxes as proposed by Biden could be difficult to implement. Further, the Biden administration is likely to push up the infrastructure agenda as it targets to build a sustainable model with a special focus on clean energy along with a revival in blue-collared jobs.

Further, a stimulus bill (higher than India’s GDP) is likely to instill confidence in the emerging as well as developed markets as the administration would probably aim for an expansionary fiscal policy.

India’s pharmaceuticals and IT stocks will be the biggest beneficiaries of a Biden administration as the President-Elect aims to increase the public healthcare expenditure along with expanding the quota for H-1B visas.

While a surge in regulations, tax burden, and wage costs could act as a deterrent to operating margin expansion, the latter is likely to get nullified by creating more demand-side measures.

Finally, globalization will experience less abrasion!

Low-interest rates attract the retail category; Festive season a booster dose

India’s top banks have started getting aggressive while lending to consumers in the hope of the latter taking the advantage of low rates to buy discretionary goods during the festive season.

The nation’s biggest banks have witnessed their retail loan portfolio grow by 3-6% sequentially after getting hit hard in the 1st quarter of FY21. Despite the uncertainty over income amidst growing unemployment, India’s retail category has resorted to borrowing with RBI’s consecutive rate cuts leading to the lowest interest rates.

While the uptick in retail loan growth is encouraging, the demand by India’s corporates is yet to pick up with the usage of credit depending upon the demand and capacity utilization.

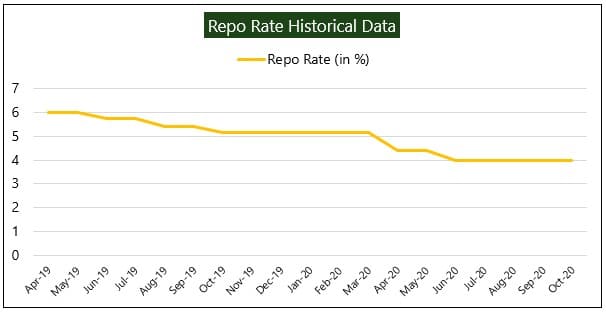

With RBI slashing the repo rate by 250 basis points in the last 2 years to 4%, the banks were forced to reduce the lending rates. Moreover, with the enactment of compulsory external benchmarking (linking of loans to an external benchmark like repo rate or bond yields) by RBI in 2019, the lenders were further induced to reduce the lending rates.

Source: Tavaga Research

With an economic slump of 24% in the quarter ending June 2020 due to the stringent lockdowns, Asia’s third-largest economy has again started to gain momentum with a range of high-frequency indicators crawling back to their pre-Covid levels.

It is imperative that unsecured loan advances could face a delinquency risk if the rising demand fails to sustain or the unemployment levels do not come down further. While the retail loans brought cheer to the lenders, the overall lending contracted by 0.2% in the quarter ending September 2020 aided by a continuing slowdown in manufacturing activities.

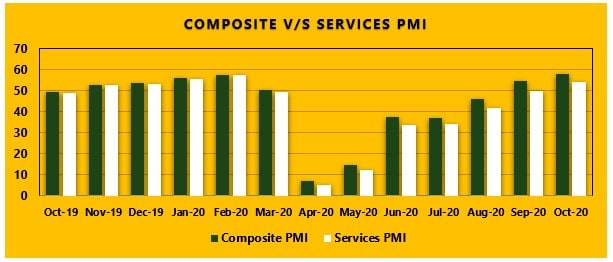

India’s Services PMI in line with the composite economic activity for the first time this fiscal

October marks the first month of expansionary services activity level this fiscal year and the first of the kind in the past eight months. Economic activity indicators captured the macro-wide disruption caused due to the coronavirus pandemic. However, the October set of numbers have made a strong case for a V-shaped revival of economic activity.

While the composite PMI crossed the 50-level mark in September, Services PMI compiled by IHS Markit followed the trend to reach a level of 54.1 in October. The Services PMI stood at 49.8 in September. The composite PMI this fiscal year was being carried by the Manufacturing PMI until September.

Source: Tavaga Research

Services PMI posting strong growth is a sign of economic recovery on the back of broader market activity. With the lifting of imposed lockdowns, domestic industries have noticed an uptick in business conducted.

Two factors will majorly affect the Services activity in the coming months: Favourable employment conditions and International business levels. The services industry is a personnel-intensive industry, making recruitment a crucial factor. If the companies in the services industry face trouble hiring staff, the growth is likely to meet constraints.

Similarly, a revival in international business levels will support the overall growth in contracts and orders. The sooner the companies can reach pre-COVID levels in terms of business attained, the quicker the companies can get over rising expenses to make the business viable. As per reports, the contraction in international demand was the slowest during the month under review. The status of vaccine release will play a significant role in taking overseas demand levels back to pre-pandemic levels.

Coming Up In The Week:

- Germany Exports – 9th November

- China Inflation Data – 10th November

- India Industrial Production and Inflation Data- 12th November

- US Inflation – 12th November

Happy Investing!